Diversification myths: Researchpost 159

Diversification myths: 14x new research on ESG and consumption, ESG data, ESG washing, ESG returns, climate risks, voting, divestments, diversification myths, anomalies, trend following, real estate and private equity

Collectibles: Researchpost 158

Collectibles: 14x new research on migration, biodiversity, forests, sustainability disclosures, ESG performance, ESG skills, ESG progress, activists and NFTs

Houseowner risks: Researchpost 157

13x new research on houseowner and job risks, migration, good lobbying, online altruism, criminal lawyers, rule of law, biodiversity, green bank risks, climate votes, private equity and innovation

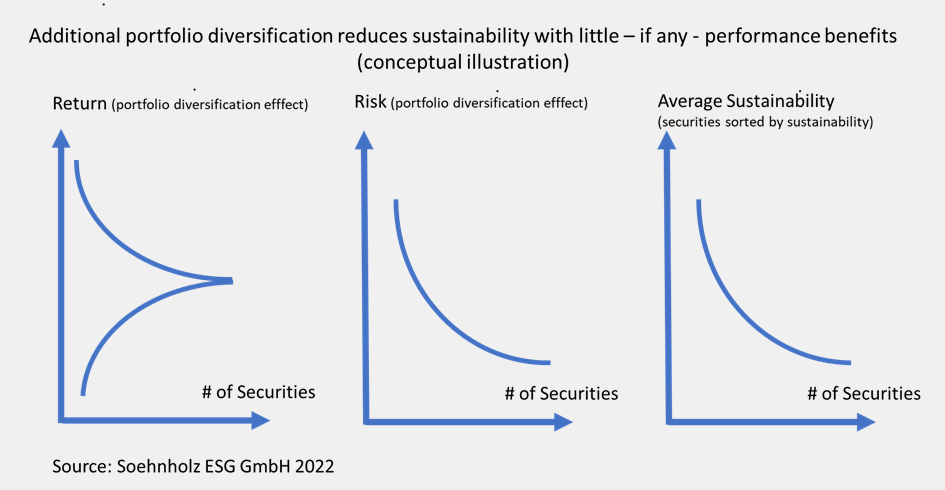

Sustainable investment = radically different?

A lower asset class diversification, more illiquid investments for large investors, more project finance, more active rather than passive mandates, significantly higher concentration within investment segments and different risk management with additional metrics and significantly less benchmark orientation.

Nachhaltige Geldanlage = Radikal anders?

Strenge Nachhaltigkeit kann zu stärkeren Unterschieden zwischen Geldanlagemandaten und radikalen Änderungen gegenüber traditionellen Mandaten führen: Geringere Diversifikation über Anlageklassen, mehr illiquide Investments für Großanleger, mehr Projektfinanzierungen, mehr aktive statt passive Mandate, erheblich höhere Konzentration innerhalb der Anlagesegmente und ein anderes Risikomanagement mit zusätzlichen Kennzahlen und erheblich geringerer Benchmarkorientierung.

Skilled fund managers – Researchpost 155

22x new research on skyscrapers, cryptos, ESG-HR, regulation, ratings, fund names, AI ESG Tools, carbon credits and accounting, impact funds, voting, Chat GPT, listed real estate, and fintechs

ESG and impact: Researchpost 154

ESG and impact: 12x new research on AI, poverty, crime, green demand, ESG risks, brown lending, green agency issues, voting, engagement, impact investing, CEO compensation, small caps etc.

Responsible derivatives? Researchpost 150

Responsible derivatives: 10x new research on migration, ESG labels, biodiversity measurement, effective shareholder voting, responsible investing mandates, green derivatives, structured products, stock market models, IPOs and alternative investments

Impact strategies: Researchpost 142

Impact strategies: 12x new research on AI, education, diversity, insiders, compensation, impact investing, collaborative engagement, voting and analysts