2023: Vereinfacht zusammengefasst haben meine Portfolioregeln in 2023 diese Wirkung gehabt: Passive Allokation und ESG gut, SDG schlecht und Trendfolge sehr schlecht…. Im Jahr 2022 hatten dagegen besonders meine Trendfolge und SDG-Portfolios gut rentiert (vgl. SDG und Trendfolge: Relativ gut in 2022).

Passives Allokations-Weltmarktportfolio 2023 mit guter Rendite

Das nicht-nachhaltige Alternatives ETF-Portfolio hat in 2023 mit 7,2% rentiert, also deutlich schlechter als Aktien insgesamt mit ca. 17%. Das regelbasierte „most passive“ Multi-Asset Weltmarkt ETF-Portfolio hat mit +9,9% trotz seines hohen Anteils an Alternatives dagegen relativ gut abgeschnitten, denn die Performance ist sogar etwas besser als die flexibler aktiver Mischfonds (+8,2%).

Eine vergleichbare Performance gilt für das ebenfalls breit diversifizierte ESG ETF-Portfolio mit +9%. Das ESG ETF-Portfolio ex Bonds lag dagegen mit +12,8% aufgrund des hohen Alternatives- und geringen Tech-Anteils erheblich hinter traditionellen Aktien-ETFs. Die Rendite ist aber ganz ähnlich wie die +12,1% traditioneller aktiv gemanagter globaler Aktienfonds. Das ESG ETF-Portfolio ex Bonds Income verzeichnete ein geringeres Plus von +9,1%. Das ist etwas schlechter als die +9,8% traditioneller Dividendenfonds.

Mit +0,8% schnitt das ESG ETF-Portfolio Bonds (EUR) ähnlich wie die +1,5% für vergleichbare traditionelle Anleihe-ETFs ab. Aktive Fonds haben jedoch +4,6% erreicht. Anders als in 2022, hat meine Trendfolge mit -1,8% für das ESG ETF-Portfolio ex Bonds Trend aber nicht gut funktioniert.

SDG ETF-Portfolio: 2023 naja

Das aus thematischen Aktien-ETFs bestehende SDG ETF-Portfolio lag mit +2,6% stark hinter traditionellen Aktienanlagen zurück und das SDG ETF-Trendfolgeportfolio zeigt mit -10% eine sehr schlechte Performance. Für thematische Investments mit ökologischem Fokus lief es allerdings in 2023 generell nicht so gut.

Um das Portfolioangebot zu straffen, werden künftig nur noch 4 ESG ETF-Portfolios aktiv angeboten: Multi-Asset (Start 2016), Aktien, renditeorientierte Anleihen und sicherheitsorientierte Anleihen (alle Start 2019). Hinzu kommen, wie gehabt, die beiden SDG ETF-Portfolios (Start 2019 und 2020).

Direkte pure ESG-Aktienportfolios OK

Das aus 30 Aktien bestehende Global Equities ESG Portfolio hat +14,6% gemacht und liegt damit besser als traditionelle aktive Fonds (+12,1%) aber hinter traditionellen Aktien-ETFs, was vor allem an den im Portfolio nicht vorhandenen Mega-Techs lag. Das nur aus 5 Titeln bestehende Global Equities ESG Portfolio S war mit +8,9% etwas schlechter, liegt aber seit dem Start in 2017 immer noch vor dem 30-Aktien Portfolio.

Das Infrastructure ESG Portfolio hat -5,1% verloren und liegt damit erheblich hinter den +0,8% traditioneller Infrastrukturfonds und den +9,2% eines traditionellen Infrastruktur-ETFs. Das Real Estate ESG Portfolio hat +7,2% gewonnen, während traditionelle globale Immobilienaktien-ETFs +6,9% und aktiv gemanagte Fonds +7,9% gewonnen haben. Das Deutsche Aktien ESG Portfolio hat +6,7% zugelegt. Das wiederum liegt erheblich hinter aktiv gemanagten traditionellen Fonds mit +15,1% und nennenswert hinter vergleichbaren ETFs mit +16,2%.

Direkte ESG plus SDG-Aktienportfolios: Nicht so gut

Das auf soziale Midcaps fokussierte Global Equities ESG SDG hat mit -0,7% im Vergleich zu allgemeinen Aktienfonds sehr schlecht abgeschnitten. Das ist vor allem auf den hohen Gesundheitsanteil zurückzuführen. Das Global Equities ESG SDG Trend Portfolio hat mit -8,4% – wie die anderen Trendfolgeportfolios – besonders schlecht abgeschnitten. Das Global Equities ESG SDG Social Portfolio hat dagegen mit +10,4% im Vergleich zum Beispiel zu Gesundheits-ETFs bzw. aktiven Fonds (-0,6 bzw. -1,0%) dagegen ziemlich gut abgeschnitten.

Aufgrund mangelnder Nachfrage werden die direkten ESG-Aktienportfolios für globale Aktien, deutsche Aktien, Infrastrukturaktien und Immobilienaktien (alle Start 2016 und 2017) künftig nicht mehr aktiv angeboten, sondern nur noch die ESG + SDG-Aktienportfolios (Start 2017 und 2022).

Fondsperformance: Nicht so gut

Mein FutureVest Equity Sustainable Development Goals R Fonds (Start 2021) zeigt nach einem im Vergleich zu anderen Portfolios sehr guten Jahr 2022 (-8,1%) in 2023 mit +0,5% eine starke Underperformance gegenüber traditionellen Aktienmärkten. Das liegt vor allem an der Branchenzusammensetzung des Portfolios mit Fokus auf Gesundheit und an den relativ hohen nachhaltigen Infrastruktur- und Immobilienanteilen (weitere Informationen wie z.B. auch den aktuellen detaillierten Engagementreport siehe FutureVest Equity Sustainable Development Goals R – DE000A2P37T6 – A2P37T). Hinzu kommt, dass die sogenannten Glorreichen 7 bewusst in keinem meiner direkten Portfolios enthalten sind (vgl. Glorreiche 7: Sind sie unsozial? – Responsible Investment Research Blog (prof-soehnholz.com)). Dafür sind das letzte Quartal 2023 mit +9,4% und vor allem der Dezember mit +9,0% besonders gut gelaufen.

Sustainable investment can be radically different from traditional investment. „Asset Allocation, Risk Overlay and Manager Selection“ is the translation of the book-title which I wrote in 2009 together with two former colleagues from FERI in Bad Homburg. Sustainability plays no role in it. My current university lecture on these topics is different.

Sustainability can play a very important role in the allocation to investment segments, manager and fund selection, position selection and also risk management. Strict sustainability can even lead to radical changes: More illiquid investments, lower asset class diversification, significantly higher concentration within investment segments, more active instead of passive mandates and different risk management. Here is why:

Central role of investment philosophy and sustainability definition for sustainable investment

Investors should define their investment philosophy as clearly as possible before they start investing. By investment philosophy, I mean the fundamental convictions of an investor, ideally a comprehensive and coherent system of such convictions (see Das-Soehnholz-ESG-und-SDG-Portfoliobuch 2023, p. 21ff.). Sustainability can be an important element of an investment philosophy.

Example: I pursue a strictly sustainable, rule-based, forecast-free investment philosophy (see e.g. Investment philosophy: Forecast fans should use forecast-free portfolios). To this end, I define comprehensive sustainability rules. I use the Policy for Responsible Investment Scoring Concept (PRISC) tool of the German Association for Asset Management and Financial Analysis (DVFA) for operationalization.

When it comes to sustainable investment, I am particularly interested in the products and services offered by the companies and organizations in which I invest or to which I indirectly provide loans. I use many strict exclusions and, above all, positive criteria. In particular, I want that the revenue or service is as compatible as possible with the Sustainable Development Goals of the United Nations (UN SDG) („SDG revenue alignment“). I also attach great importance to low absolute environmental, social and governance (ESG) risks. However, I only give a relatively low weighting to the opportunities to change investments („investor impact“) (see The Soehnholz ESG and SDG Portfolio Book 2023, p. 141ff). I try to achieve impact primarily through shareholder engagement, i.e. direct sustainability communication with companies.

Other investors, for whom impact and their own opportunities for change are particularly important, often attach great importance to so-called additionality. This means, that the corresponding sustainability improvements only come about through their respective investments. If an investor finances a new solar or wind park, this is considered additional and therefore particularly sustainable. When investing money on stock exchanges, securities are only bought by other investors and no money flows to the issuers of the securities – except in the case of relatively rare new issues. The purchase of listed bonds or shares in solar and wind farm companies is therefore not considered an impact investment by additionality supporters.

Sustainable investment and asset allocation: many more unlisted or alternative investments and more bonds?

In extreme cases, an investment philosophy focused on additionality would mean investing only in illiquid assets. Such an asset allocation would be radically different from today’s typical investments.

Better no additional allocation to illiquid investments?

Regarding additionality, investor and project impact must be distinguished. The financing of a new wind farm is not an additional investment, if other investors would also finance the wind farm on their own. This is not atypical. There is often a so-called capital overhang for infrastructure and private equity investments. This means, that a lot of money has been raised via investment funds and is competing for investments in such projects.

Even if only one fund is prepared to finance a sustainable project, the investment in such a fund would not be additional if other investors are willing to commit enough money to this fund to finance all planned investments. It is not only funds from renowned providers that often have more potential subscriptions from potential investors than they are willing to accept. Investments in such funds cannot necessarily be regarded as additional. On the other hand, there is clear additionality for investments that no one else wants to make. However, whether such investments will generate attractive performance is questionable.

Illiquid investments are also far from suitable for all investors, as they usually require relatively high minimum investments. In addition, illiquid investments are usually only invested gradually, and liquidity must be held for uncertain capital calls in terms of timing and amount. In addition, illiquid investments are usually considerably more expensive than comparable liquid investments. Overall, illiquid investments therefore have hardly any higher return potential than liquid investments. On the other hand, mainly due to the methods of their infrequent valuations, they typically exhibit low fluctuations. However, they are sometimes highly risky due to their high minimum investments and, above all, illiquidity.

In addition, illiquid investments lack an important so-called impact channel, namely individual divestment opportunities. While liquid investments can be sold at any time if sustainability requirements are no longer met, illiquid investments sometimes have to remain invested for a very long time. Divestment options are very important to me: I have sold around half of my securities in recent years because their sustainability has deteriorated (see: Divestments: 49 bei 30 Aktien meines Artikel 9 Fonds).

Sustainability advantages for (corporate) bonds over equities?

Liquid investment segments can differ, too, in terms of impact opportunities. Voting rights can be exercised for shares, but not for bonds and other investment segments. However, shareholder meetings at which voting is possible rarely take place. In addition, comprehensive sustainability changes are rarely put to the vote. If they are, they are usually rejected (see 2023 Proxy Season Review – Minerva).

I am convinced that engagement in the narrower sense can be more effective than exercising voting rights. And direct discussions with companies and organizations to make them more sustainable are also possible for bond buyers.

Irrespective of the question of liquidity or stock market listing, sustainable investors may prefer loans to equity because loans can be granted specifically for social and ecological projects. In addition, payouts can be made dependent on the achievement of sustainable milestones. However, the latter can also be done with private equity investments, but not with listed equity investments. However, if ecological and social projects would also be carried out without these loans and only replace traditional loans, the potential sustainability advantage of loans over equity is put into perspective.

Loans are usually granted with specific repayment periods. Short-term loans have the advantage that it is possible to decide more often whether to repeat loans than with long-term loans, provided they cannot be repaid early. This means that it is usually easier to exit a loan that is recognized as not sustainable enough than a private equity investment. This is a sustainability advantage. In addition, smaller borrowers and companies can probably be influenced more sustainably, so that government bonds, for example, have less sustainability potential than corporate loans, especially when it comes to relatively small companies.

With regard to real estate, one could assume that loans or equity for often urgently needed residential or social real estate can be considered more sustainable than for commercial real estate. The same applies to social infrastructure compared to some other infrastructure segments. On the other hand, some market observers criticize the so-called financialization of residential real estate, for example, and advocate public rather than private investments (see e.g. Neue Studie von Finanzwende Recherche: Rendite mit der Miete). Even social loans such as microfinance in the original sense are criticized, at least when commercial (interest) interests become too strong and private debt increases too much.

While renewable raw materials can be sustainable, non-industrially used precious metals are usually considered unsustainable due to the mining conditions. Crypto investments are usually considered unsustainable due to their lack of substance and high energy consumption.

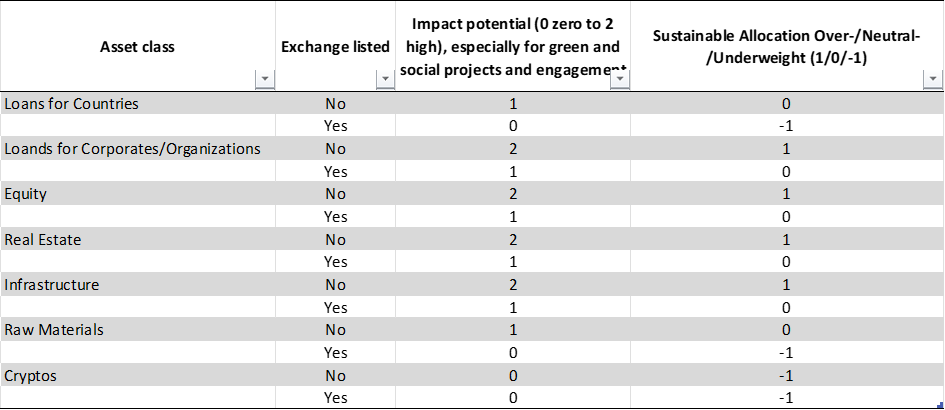

Assuming potential additionality for illiquid investments and an impact primarily via investments with an ecological or social focus, the following simplified assessment of the investment segment can be made from a sustainability perspective:

Sustainable investment: Potential weighting of investment segments assuming additionality for illiquid investments:

Source: Soehnholz ESG GmbH 2023

Investors should create their own such classification, as this is crucial for their respective sustainable asset allocation.

Taking into account minimum capital investment and costs as well as divestment and engagement opportunities, I only invest in listed investments, for example. However, in the case of multi-billion assets with direct sustainability influence on investments, I would consider additional illiquid investments.

Sustainable investment and manager/fund selection: more active investments again?

Scientific research shows that active portfolio management usually generates lower returns and often higher risks than passive investments. With very low-cost ETFs, you can invest in thousands of securities. It is therefore no wonder that so-called passive investments have become increasingly popular in recent years.

Diversification is often seen as the only „free lunch“ in investing. But diversification often has no significant impact on returns or risks: With more than 20 to 30 securities from different countries and sectors, no better returns and hardly any lower risks can be expected than with hundreds of securities. In other words, the marginal benefit of additional diversification decreases very quickly.

But if you start with the most sustainable 10 to 20 securities and diversify further, the average sustainability can fall considerably. This means that strictly sustainable investment portfolios should be concentrated rather than diversified. Concentration also has the advantage of making voting and other forms of engagement easier and cheaper. Divestment threats can also be more effective if a lot of investor money is invested in just a few securities.

Sustainability policies can vary widely. This can be seen, among other things, in the many possible exclusions from potential investments. For example, animal testing can be divided into legally required, medically necessary, cosmetic and others. Some investors want to consistently exclude all animal testing. Others want to continue investing in pharmaceutical companies and may therefore only exclude „other“ animal testing. And investors who want to promote the transition from less sustainable companies, for example in the oil industry, to more sustainability will explicitly invest in oil companies (see ESG Transition Bullshit?).

Indices often contain a large number of securities. However, consistent sustainability argues in favor of investments in concentrated, individual and therefore mostly index-deviating actively managed portfolios. Active, though, is not meant in the sense of a lot of trading. In order to be able to exert influence by exercising voting rights and other forms of engagement, longer rather than shorter holding periods for investments make sense.

Still not enough consistently sustainable ETF offerings

When I started my own company in early 2016, it was probably the world’s first provider of a portfolio of the most consistently sustainable ETFs possible. But even the most sustainable ETFs were not sustainable enough for me. This was mainly due to insufficient exclusions and the almost exclusive use of aggregated best-in-class ESG ratings. However, I have high minimum requirements for E, S and G separately (see Glorious 7: Are they anti-social?). I am also not interested in the best-rated companies within sectors that are unattractive from a sustainability perspective (best-in-class). I want to invest in the best-performing stocks regardless of sector (best-in-universe). However, there are still no ETFs for such an approach. In addition, there are very few ETFs that use strict ESG criteria and also strive for SDG compatibility.

Even in the global Socially Responsible Investment Paris Aligned Benchmarks, which are particularly sustainable, there are still several hundred stocks from a large number of sectors and countries. In contrast, there are active global sustainable funds with just 30 stocks, which is potentially much more sustainable (see 30 stocks, if responsible, are all I need).

Issuers of sustainable ETFs often exercise sustainable voting rights and even engage, even if only to a small extent. However, most providers of active investments do no better (see e.g. 2023 Proxy Season Review – Minerva). Notably, index-following investments typically do not use the divestment impact channel because they want to replicate indices as directly as possible.

Sustainable investment and securities selection: fewer standard products and more individual mandates or direct indexing?

If there are no ETFs that are sustainable enough, you should look for actively managed funds, award sustainable mandates to asset managers or develop your own portfolios. However, actively managed concentrated funds with a strict ESG plus impact approach are still very rare. This also applies to asset managers who could implement such mandates. In addition, high minimum investments are often required for customized mandates. Individual sustainable portfolio developments, on the other hand, are becoming increasingly simple.

Numerous providers currently offer basic sustainability data for private investors at low cost or even free of charge. Financial technology developments such as discount (online) brokers, direct indexing and trading in fractional shares as well as voting tools help with the efficient and sustainable implementation of individual portfolios. However, the variety of investment opportunities and data qualities are not easy to analyze.

It would be ideal if investors could also take their own sustainability requirements into account on the basis of a curated universe of particularly sustainable securities and then have them automatically implemented and rebalanced in their portfolios (see Custom ESG Indexing Can Challenge Popularity Of ETFs (asiafinancial.com). In addition, they could use modern tools to exercise their voting rights according to their individual sustainability preferences. Sustainability engagement with the securities issuers can be carried out by the platform provider.

Risk management: much more tracking error and ESG risk monitoring?

For sustainable investments, sustainability metrics are added to traditional risk metrics. These are, for example, ESG ratings, emissions values, principal adverse indicators, do-no-significant-harm information, EU taxonomy compliance or, as in my case, SDG compliance and engagement success.

Sustainable investors have to decide how important the respective criteria are for them. I use sustainability criteria not only for reporting, but also for my rule-based risk management. This means that I sell securities if ESG or SDG requirements are no longer met (see Divestments: 49 bei 30 Aktien meines Artikel 9 Fonds).

The ESG ratings I use summarize environmental, social and governance risks. These risks are already important today and will become even more important in the future, as can be seen from greenwashing and reputational risks, for example. Therefore, they should not be missing from any risk management system. SDG compliance, on the other hand, is only relevant for investors who care about how sustainable the products and services of their investments are.

Voting rights and engagement have not usually been used for risk management up to now. However, this may change in the future. For example, I check whether I should sell shares if there is an inadequate response to my engagement. An inadequate engagement response from companies may indicate that companies are not listening to good suggestions and thus taking unnecessary risks that can be avoided through divestments.

Traditional investors often measure risk by the deviation from the target allocation or benchmark. If the deviation exceeds a predefined level, many portfolios have to be realigned closer to the benchmark. If you want to invest in a particularly sustainable way, you have to have higher rather than lower traditional benchmark deviations (tracking error) or you should do without tracking error figures altogether.

In theory, sustainable indices could be used as benchmarks for sustainable portfolios. However, as explained above, sustainability requirements can be very individual and, in my opinion, there are no strict enough sustainable standard benchmarks yet.

Sustainability can therefore lead to new risk indicators as well as calling old ones into question and thus also lead to significantly different risk management.

Summary and outlook: Much more individuality?

Individual sustainability requirements play a very important role in the allocation to investment segments, manager and fund selection, position selection and risk management. Strict sustainability can lead to greater differences between investment mandates and radical changes to traditional mandates: A lower asset class diversification, more illiquid investments for large investors, more project finance, more active rather than passive mandates, significantly higher concentration within investment segments and different risk management with additional metrics and significantly less benchmark orientation.

Some analysts believe that sustainable investment leads to higher risks, higher costs and lower returns. Others expect disproportionately high investments in sustainable investments in the future. This should lead to a better performance of such investments. My approach: I try to invest as sustainably as possible and I expect a normal market return in the medium term with lower risks compared to traditional investments.

First published in German on www.prof-soehnholz.com on Dec. 30th, 2023. Initial version translated by Deepl.com

Nachhaltige Geldanlage kann radikal anders sein als traditionelle. „Asset Allocation, Risiko-Overlay und Manager-Selektion: Das Diversifikationsbuch“ heißt das Buch, dass ich 2009 mit ehemaligen Kollegen der Bad Homburger FERI geschrieben habe. Nachhaltigkeit spielt darin keine Rolle. In meiner aktuellen Vorlesung zu diesen Themen ist das anders. Nachhaltigkeit kann eine sehr wichtige Rolle spielen für die Allokation auf Anlagesegmente, die Manager- bzw. Fondsselektion, die Positionsselektion und auch das Risikomanagement (Hinweis: Um die Lesbarkeit zu verbessern, gendere ich nicht).

Strenge Nachhaltigkeit kann sogar zu radikalen Änderungen führen: Mehr illiquide Investments, erheblich höhere Konzentration innerhalb der Anlagesegmente, mehr aktive statt passive Mandate und ein anderes Risikomanagement. Im Folgenden erkläre ich, wieso:

Zentrale Rolle von Investmentphilosophie und Nachhaltigkeitsdefinition für die nachhaltige Geldanlage

Dafür starte ich mit der Investmentphilosophie. Unter Investmentphilosophie verstehe ich die grundsätzlichen Überzeugungen eines Geldanlegers, idealerweise ein umfassendes und kohärentes System solcher Überzeugungen (vgl. Das-Soehnholz-ESG-und-SDG-Portfoliobuch 2023, S. 21ff.). Nachhaltigkeit kann ein wichtiges Element einer Investmentphilosophie sein. Anleger sollten ihre Investmentphilosophie möglichst klar definieren, bevor sie mit der Geldanlage beginnen.

Beispiel: Ich verfolge eine konsequent nachhaltige regelbasiert-prognosefreie Investmentphilosophie. Dafür definiere ich umfassende Nachhaltigkeitsregeln. Zur Operationalisierung nutze ich das Policy for Responsible Investment Scoring Concept (PRISC) Tool der Deutschen Vereinigung für Asset Management und Finanzanalyse (DVFA, vgl. Standards – DVFA e. V. – Der Berufsverband der Investment Professionals).

Für die nachhaltige Geldanlage ist mir vor allem wichtig, was für Produkte und Services die Unternehmen und Organisationen anbieten, an denen ich mich beteilige oder denen ich indirekt Kredite zur Verfügung stelle. Dazu nutze ich viele strenge Ausschlüsse und vor allem Positivkriterien. Dabei wird vor allem der Umsatz- bzw. Serviceanteil betrachtet, der möglichst gut mit Nachhaltigen Entwicklungszielen der Vereinten Nationen (UN SDG) vereinbar ist („SDG Revenue Alignment“). Außerdem lege ich viel Wert auf niedrige absolute Umwelt-, Sozial- und Governance-Risiken (ESG). Meine Möglichkeiten zur Veränderung von Investments („Investor Impact“) gewichte ich aber nur relativ niedrig (vgl. Das-Soehnholz-ESG-und-SDG-Portfoliobuch 2023, S. 141ff). Impact möchte ich dabei vor allem über Shareholder Engagement ausüben, also direkte Nachhaltigkeitskommunikation mit Unternehmen.

Andere Anleger, denen Impact- bzw. eigene Veränderungsmöglichkeiten besonders wichtig sind, legen oft viel Wert auf sogenannte Additionalität bzw. Zusätzlichkeit. Das bedeutet, dass die entsprechenden Nachhaltigkeitsverbesserungen nur durch ihre jeweiligen Investments zustande gekommen sind. Wenn ein Anleger einen neuen Solar- oder Windparkt finanziert, gilt das als additional und damit als besonders nachhaltig. Bei Geldanlagen an Börsen werden Wertpapiere nur anderen Anlegern abgekauft und den Herausgebern der Wertpapiere fließt – außer bei relativ seltenen Neuemissionen – kein Geld zu. Der Kauf börsennotierter Anleihen oder Aktien von Solar- und Windparkunternehmen gilt bei Additionalitätsanhängern deshalb nicht als Impact Investment.

Nachhaltige Geldanlage und Asset Allokation: Viel mehr nicht-börsennotierte bzw. alternative Investments und mehr Anleihen?

Eine additionalitätsfokussierte Investmentphilosophie bedeutet demnach im Extremfall, nur noch illiquide zu investieren. Die Asset Allokation wäre radikal anders als heute typische Geldanlagen.

Lieber keine Mehrallokation zu illiquiden Investments?

Aber wenn Additionalität so wichtig ist, dann muss man sich fragen, welche Art von illiquiden Investments wirklich Zusätzlichkeit bedeutet. Dazu muss man Investoren- und Projektimpact trennen. Die Finanzierung eines neuen Windparks ist aus Anlegersicht dann nicht zusätzlich, wenn andere Anleger den Windpark auch alleine finanzieren würden. Das ist durchaus nicht untypisch. Für Infrastruktur- und Private Equity Investments gibt es oft einen sogenannten Kapitalüberhang. Das bedeutet, dass über Fonds sehr viel Geld eingesammelt wurde und um Anlagen in solche Projekte konkurriert.

Selbst wenn nur ein Fonds zur Finanzierung eines nachhaltgien Projektes bereit ist, wäre die Beteiligung an einem solchen Fonds aus Anlegersicht dann nicht additional, wenn alternativ andere Anleger diese Fondsbeteiligung kaufen würden. Nicht nur Fonds renommierter Anbieter haben oft mehr Anfragen von potenziellen Anlegern als sie akzeptieren wollen. Investments in solche Fonds kann man nicht unbedingt als additional ansehen. Klare Additionalität gibt es dagegen für Investments, die kein anderer machen will. Ob solche Investments aber attraktive Performances versprechen, ist fragwürdig.

Illiquide Investments sind zudem längst nicht für alle Anleger geeignet, denn sie erfordern meistens relativ hohe Mindestinvestments. Hinzu kommt, dass man bei illiquiden Investments in der Regel erst nach und nach investiert und Liquidität in Bezug auf Zeitpunkt und Höhe unsichere Kapitalabrufe bereithalten muss. Außerdem sind illiquide meistens erheblich teurer als vergleichbare liquide Investments. Insgesamt haben damit illiquide Investments kaum höhere Renditepotenziale als liquide Investments. Durch die Art ihrer Bewertungen zeigen sie zwar geringe Schwankungen. Sie sind durch ihre hohen Mindestinvestments und vor allem Illiquidität aber teilweise hochriskant.

Hinzu kommt, dass illiquiden Investments ein wichtiger sogenannter Wirkungskanal fehlt, nämlich individuelle Divestmentmöglichkeiten. Während liquide Investments jederzeit verkauft werden können wenn Nachhaltigkeitsanforderungen nicht mehr erfüllt werden, muss man bei illiquiden Investments teilweise sehr lange weiter investiert bleiben. Divestmentmöglichkeiten sind sehr wichtig für mich: Ich habe in den letzten Jahren jeweils ungefähr die Hälfte meiner Wertpapiere verkauft, weil sich ihre Nachhaltigkeit verschlechtert hat (vgl. Divestments: 49 bei 30 Aktien meines Artikel 9 Fonds – Responsible Investment Research Blog (prof-soehnholz.com)).

Nachhaltigkeitsvorteile für (Unternehmens-)Anleihen gegenüber Aktien?

Auch liquide Anlagesegmente können sich in Bezug auf Impactmöglichkeiten unterscheiden. Für Aktien kann man Stimmrechte ausüben (Voting), für Anleihen und andere Anlagesegmente nicht. Allerdings finden nur selten Aktionärsversammlungen statt, zu denen man Stimmrechte ausüben kann. Zudem stehen nur selten umfassende Nachhaltigkeitsveränderungen zur Abstimmung. Falls das dennoch der Fall ist, werden sie meistens abgelehnt (vgl. 2023 Proxy Season Review – Minerva-Manifest).

Ich bin überzeugt, dass Engagement im engeren Sinn wirkungsvoller sein kann als Stimmrechtsausübung. Und direkte Diskussionen mit Unternehmen und Organisationen, um diese nachhaltiger zu machen, sind auch für Käufer von Anleihen möglich.

Unabhängig von der Frage der Liquidität bzw. Börsennotiz könnten nachhaltige Anleger Kredite gegenüber Eigenkapital bevorzugen, weil Kredite speziell für soziale und ökologische Projekte vergeben werden können. Außerdem können Auszahlungen von der Erreichung von nachhaltigen Meilensteinen abhängig gemacht werden können. Letzteres kann bei Private Equity Investments aber ebenfalls gemacht werden, nicht jedoch bei börsennotierten Aktieninvestments. Wenn ökologische und soziale Projekte aber auch ohne diese Kredite durchgeführt würden und nur traditionelle Kredite ersetzen, relativiert sich der potenzielle Nachhaltigkeitsvorteil von Krediten gegenüber Eigenkapital.

Allerdings werden Kredite meist mit konkreten Rückzahlungszeiten vergeben. Kurz laufende Kredite haben dabei den Vorteil, dass man öfter über die Wiederholung von Kreditvergaben entscheiden kann als bei langlaufenden Krediten, sofern man sie nicht vorzeitig zurückbezahlt bekommen kann. Damit kann man aus einer als nicht nachhaltig genug erkannter Kreditvergabe meistens eher aussteigen als aus einer privaten Eigenkapitalvergabe. Das ist ein Nachhaltigkeitsvorteil. Außerdem kann man kleinere Kreditnehmer und Unternehmen wohl besser nachhaltig beeinflussen, so dass zum Beispiel Staatsanleihen weniger Nachhaltigkeitspotential als Unternehmenskredite haben, vor allem wenn es sich dabei um relativ kleine Unternehmen handelt.

In Bezug auf Immobilien könnte man annehmen, dass Kredite oder Eigenkapital für oft dringend benötigte Wohn- oder Sozialimmobilien als nachhaltiger gelten können als für Gewerbeimmobilien. Ähnliches gilt für Sozialinfrastruktur gegenüber manch anderen Infrastruktursegmenten. Andererseits kritisieren manche Marktbeobachter die sogenannte Finanzialisierung zum Beispiel von Wohnimmobilien (vgl. Neue Studie von Finanzwende Recherche: Rendite mit der Miete) und plädieren grundsätzlich für öffentliche statt private Investments. Selbst Sozialkredite wie Mikrofinanz im ursprünglichen Sinn wird zumindest dann kritisiert, wenn kommerzielle (Zins-)Interessen zu stark werden und private Verschuldungen zu stark steigen.

Während nachwachsende Rohstoffe nachhaltig sein können, gelten nicht industriell genutzte Edelmetalle aufgrund der Abbaubedingungen meistens als nicht nachhaltig. Kryptoinvestments werden aufgrund fehlender Substanz und hoher Energieverbräuche meistens als nicht nachhaltig beurteilt.

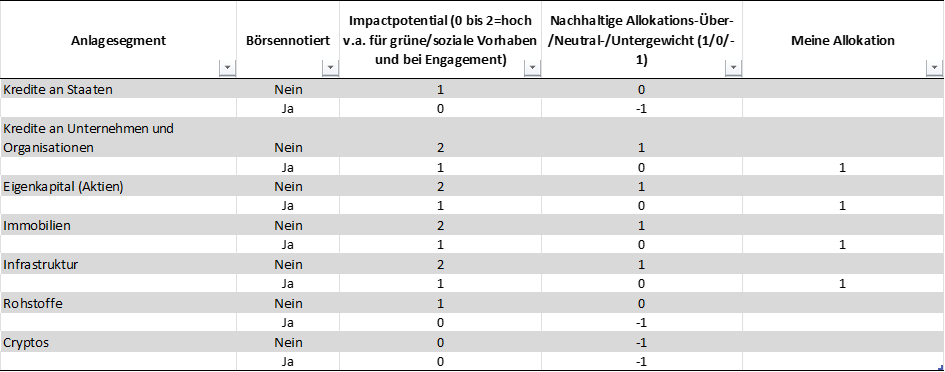

Bei der Annahme von potenzieller Additionalität für illiquide Investments und Wirkung vor allem über Investments mit ökologischem bzw. sozialem Bezug kann man zu der folgenden vereinfachten Anlagesegmentbeurteilung aus Nachhaltigkeitssicht kommen:

Nachhaltige Geldanlage: Potenzielle Gewichtung von Anlagesegmenten bei Annahme von Additionalität für illiquide Investmentsund meine Allokation

Quelle: Eigene Darstellung

Anleger sollten sich ihre eigene derartige Klassifikation erstellen, weil diese entscheidend für ihre jeweilige nachhaltige Asset Allokation ist. Unter Berücksichtigung von Mindestkapitaleinsatz und Kosten sowie Divestment- und Engagementmöglichkeiten investiere ich zum Beispiel nur in börsennotierte Investments. Bei einem Multi-Milliarden Vermögen mit direkten Nachhaltigkeits-Einflussmöglichkeiten auf Beteiligungen würde ich zusätzliche illiquide Investments aber in Erwägung ziehen. Insgesamt kann strenge Nachhaltigkeit also auch zu wesentlich geringerer Diversifikation über Anlageklassen führen.

Nachhaltige Geldanlage und Manager-/Fondsselektion: Wieder mehr aktive Investments?

Wissenschaftliche Forschung zeigt, dass aktives Portfoliomanagement meistens geringe Renditen und oft auch höhere Risiken als passive Investments einbringt. Mit sehr günstigen ETFs kann man in tausende von Wertpapieren investieren. Es ist deshalb kein Wunder, dass in den letzten Jahren sogenannte passive Investments immer beliebter geworden sind.

Diversifikation gilt oft als der einzige „Free Lunch“ der Kapitalanlage. Aber Diversifikation hat oft keinen nennenswerten Einfluss auf Renditen oder Risiken. Anders ausgedrückt: Mit mehr als 20 bis 30 Wertpapieren aus unterschiedlichen Ländern und Branchen sind keine besseren Renditen und auch kaum niedrigere Risiken zu erwarten als mit hunderten von Wertpapieren. Anders ausgedrückt: Der Grenznutzen zusätzlicher Diversifikation nimmt sehr schnell ab.

Aber wenn man aber mit den nachhaltigsten 10 bis 20 Wertpapiern startet und weiter diversifiziert, kann die durchschnittliche Nachhaltigkeit erheblich sinken. Das bedeutet, dass konsequent nachhaltige Geldanlageportfolios eher konzentriert als diversifiziert sein sollten. Konzentration hat auch den Vorteil, dass Stimmrechtsausübungen und andere Formen von Engagement einfacher und kostengünstiger werden. Divestment-Androhungen können zudem wirkungsvoller sein, wenn viel Anlegergeld in nur wenige Wertpapiere investiert wird.

Nachhaltigkeitspolitiken können sehr unterschiedlich ausfallen. Das zeigt sich unter anderem bei den vielen möglichen Ausschlüssen von potenziellen Investments. So kann man zum Beispiel Tierversuche in juristisch vorgeschriebene, medizinisch nötige, kosmetische und andere unterscheiden. Manche Anleger möchten alle Tierversuche konsequent ausschließen. Andere wollen weiterhin in Pharmaunternehmen investieren und schließen deshalb vielleicht nur „andere“ Tierversuche aus. Und Anleger, welche die Transition von wenig nachhaltigen Unternehmen zum Beispiel der Ölbranche zu mehr Nachhaltigkeit fördern wollen, werden explizit in Ölunternehmen investieren (vgl. ESG Transition Bullshit? – Responsible Investment Research Blog (prof-soehnholz.com)).

Indizes enthalten oft sehr viele Wertpapiere. Konsequente Nachhaltigkeit spricht aber für Investments in konzentrierte, individuelle und damit meist indexabweichende aktiv gemanagte Portfolios. Dabei ist aktiv nicht im Sinne von viel Handel gemeint. Um über Stimmrechtsausübungen und andere Engagementformen Einfluss ausüben zu können, sind eher längere als kürzere Haltedauern von Investments sinnvoll.

Immer noch nicht genug konsequent nachhaltige ETF-Angebote

Bei der Gründung meines eigenen Unternehmens Anfang 2016 war ich wahrscheinlich weltweit der erste Anbieter eines Portfolios aus möglichst konsequent nachhaltigen ETFs. Aber auch die nachhaltigsten ETFs waren mir nicht nachhaltig genug. Grund waren vor allem unzureichende Ausschlüsse und die fast ausschließliche Nutzung von aggregierten Best-in-Class ESG-Ratings. Ich habe aber hohe Mindestanforderungen an E, S und G separat (vgl. Glorreiche 7: Sind sie unsozial? – Responsible Investment Research Blog (prof-soehnholz.com). Ich interessiere mich auch nicht für die am besten geraten Unternehmen innerhalb aus Nachhaltigkeitssicht unattraktiven Branchen (Best-in-Class). Ich möchte branchenunabhängig in die am besten geraten Aktien investieren (Best-in-Universe). Dafür gibt es aber auch heute noch keine ETFs. Außerdem gibt es sehr wenige ETFs, die strikte ESG-Kriterien nutzen und zusätzlich SDG-Vereinbarkeit anstreben.

Auch in den in besonders konsequent nachhaltigen globalen Socially Responsible Paris Aligned Benchmarks befinden sich noch mehrere hundert Aktien aus sehr vielen Branchen und Ländern. Aktive globale nachhaltige Fonds gibt es dagegen schon mit nur 30 Aktien, also potenziell erheblich nachhaltiger (vgl. 30 stocks, if responsible, are all I need – Responsible Investment Research Blog (prof-soehnholz.com)).

Emittenten nachhaltiger ETFs üben oft nachhaltige Stimmrechtsausübungen und sogar Engagement aus, wenn auch nur in geringem Umfang. Das machen die meisten Anbieter aktiver Investments aber auch nicht besser (vgl. z.B. 2023 Proxy Season Review – Minerva-Manifest). Indexfolgende Investments nutzen aber typischerweise den Impactkanal Divestments nicht, weil sie Indizes möglichst direkt nachbilden wollen.

Nachhaltige Geldanlage und Wertpapierselektion: Weniger Standardprodukte und mehr individuelle Mandate oder Direct Indexing?

Wenn es keine ETFs gibt, die nachhaltig genug sind, sollte man sich aktiv gemanagte Fonds suchen, nachhaltige Mandate an Vermögensverwalter vergeben oder seine Portfolios selbst entwickeln. Aktiv gemanagte konzentrierte Fonds mit strengem ESG plus Impactansatz sind aber noch sehr selten. Das gilt auch für Vermögensverwalter, die solche Mandate umsetzen könnten. Außerdem werden für maßgeschneiderte Mandate oft hohe Mindestanlagen verlangt. Individuelle nachhaltige Portfolioentwicklungen werden dagegen zunehmend einfacher.

Basis-Nachhaltigkeitsdaten werden aktuell von zahlreichen Anbietern für Privatanleger kostengünstig oder sogar kostenlos angeboten. Finanztechnische Entwicklungen wie Discount-(Online-)Broker, Direct Indexing und Handel mit Bruchstücken von Wertpapieren sowie Stimmrechtsausübungstools helfen bei der effizienten und nachhaltigen Umsetzung von individuellen Portfolios. Schwierigkeiten bereiten dabei eher die Vielfalt an Investmentmöglichkeiten und mangelnde bzw. schwer zu beurteilende Datenqualität.

Ideal wäre, wenn Anleger auf Basis eines kuratierten Universums von besonders nachhaltigen Wertpapieren zusätzlich eigene Nachhaltigkeitsanforderungen berücksichtigen können und dann automatisiert in ihren Depots implementieren und rebalanzieren lassen (vgl. Custom ESG Indexing Can Challenge Popularity Of ETFs (asiafinancial.com). Zusätzlich könnten sie mit Hilfe moderner Tools ihre Stimmrechte nach individuellen Nachhaltigkeitsvorstellungen ausüben. Direkte Nachhaltigkeitskommunikation mit den Wertpapieremittenten kann durch den Plattformanbieter erfolgen.

Risikomanagement: Viel mehr Tracking-Error und ESG-Risikomonitoring?

Für nachhaltige Geldanlagen kommen zusätzlich zu traditionellen Risikokennzahlen Nachhaltigkeitskennzahlen hinzu, zum Beispiel ESG-Ratings, Emissionswerte, Principal Adverse Indicators, Do-No-Significant-Harm-Informationen, EU-Taxonomievereinbarkeit oder, wie in meinem Fall, SDG-Vereinbarkeiten und Engagementerfolge.

Nachhaltige Anleger müssen sich entscheiden, wie wichtig die jeweiligen Kriterien für sie sind. Ich nutze Nachhaltigkeitskriterien nicht nur für das Reporting, sondern auch für mein regelgebundenes Risikomanagement. Das heißt, dass ich Wertpapiere verkaufe, wenn ESG- oder SDG-Anforderungen nicht mehr erfüllt werden.

Die von mir genutzten ESG-Ratings messen Umwelt-, Sozial- und Unternehmensführungsrisiken. Diese Risiken sind heute schon wichtig und werden künftig noch wichtiger, wie man zum Beispiel an Greenwashing- und Reputationsrisiken sehen kann. Deshalb sollten sie in keinem Risikomanagement fehlen. SDG-Anforderungserfüllung ist hingegen nur für Anleger relevant, denen wichtig ist, wie nachhaltig die Produkte und Services ihrer Investments sind.

Stimmrechtsausübungen und Engagement wurden bisher meistens nicht für das Risikomanagement genutzt. Das kann sich künftig jedoch ändern. Ich prüfe zum Beispiel, ob ich Aktien bei unzureichender Reaktion auf mein Engagement verkaufen sollte. Eine unzureichende Engagementreaktion von Unternehmen weist möglicherweise darauf hin, dass Unternehmen nicht auf gute Vorschläge hören und damit unnötige Risiken eingehen, die man durch Divestments vermeiden kann.

Traditionelle Geldanleger messen Risiko oft mit der Abweichung von der Soll-Allokation bzw. Benchmark. Wenn die Abweichung einen vorher definierten Grad überschreitet, müssen viele Portfolios wieder benchmarknäher ausgerichtet werden. Für nachhaltige Portfolios werden dafür auch nachhaltige Indizes als Benchmark genutzt. Wie oben erläutert, können Nachhaltigkeitsanforderungen aber sehr individuell sein und es gibt meiner Ansicht nach viel zu wenige strenge nachhaltige Benchmarks. Wenn man besonders nachhaltig anlegen möchte, muss man dementsprechend höhere statt niedrigere Benchmarkabweichungen (Tracking Error) haben bzw. sollte ganz auf Tracking Error Kennzahlen verzichten.

Nachhaltigkeit kann also sowohl zu neuen Risikokennzahlen führen als auch alte in Frage stellen und damit auch zu einem erheblich anderen Risikomanagement führen.

Nachhaltige Geldanlage – Zusammenfassung und Ausblick: Viel mehr Individualität?

Individuelle Nachhaltigkeitsanforderungen spielen eine sehr wichtige Rolle für die Allokation auf Anlagesegmente, die Manager- bzw. Fondsselektion, die Positionsselektion und auch das Risikomanagement. Strenge Nachhaltigkeit kann zu stärkeren Unterschieden zwischen Geldanlagemandaten und radikalen Änderungen gegenüber traditionellen Mandaten führen: Geringere Diversifikation über Anlageklassen, mehr illiquide Investments für Großanleger, mehr Projektfinanzierungen, mehr aktive statt passive Mandate, erheblich höhere Konzentration innerhalb der Anlagesegmente und ein anderes Risikomanagement mit zusätzlichen Kennzahlen und erheblich geringerer Benchmarkorientierung.

Manche Analysten meinen, nachhaltige Geldanlage führt zu höheren Risiken, höheren Kosten und niedrigeren Renditen. Andere erwarten zukünftig überproportional hohe Anlagen in nachhaltige Investments. Das sollte zu einer besseren Performance solcher Investments führen. Meine Einstellung: Ich versuche so nachhaltig wie möglich zu investieren und erwarte dafür mittelfristig eine marktübliche Rendite mit niedrigeren Risiken im Vergleich zu traditionellen Investments.

ESG research criticism: 13x new research on e-commerce, petrochemical and corruption problems, good and average sustainable performance, high transition risks, EU Taxonomy, Greenium, climate disaster effects, good investment constraints and private equity benchmarks (# shows SSRN full paper downloads as of Dec. 14th, 2023)

Social and ecological research (ESG research criticism)

Brown e-commerce: Product flows and GHG emissions associated with consumer returns in the EU by Rotem Roichman, Tamar Makov, Benjamin Sprecher, Vered Blass, and Tamar Meshulam as of Dec. 6th, 2023 (#5):“Building on a unique dataset covering over 630k returned apparel items in the EU … Our results indicate that 22%-44% of returned products never reach another consumer. Moreover, GHG emissions associated with the production and distribution of unused returns can be 2-14 times higher than post-return transport, packaging, and processing emissions combined“ (abstract).

US financed European petrochemicals:Toxic Footprints Europe by Planet Tracker as of December 2023: “Petrochemicals, which provide feedstocks for numerous products embedded in the global economy, carry a significant environmental footprint. One of the most important is toxic emissions. The financial market appears largely unconcerned by toxic emissions. This could be for several reasons: • perhaps because they are viewed as an unpriced pollutant or investors’ focus remains on carbon rather than other discharges or for those monitoring the plastic industry the spotlight is on plastic waste rather than toxic releases. In the Trilateral Chemical Region of Europe – an area consisting of Flanders (Belgium), North Rhine-Westphalia (Germany), Planet Tracker identified 1,093 facilities …. These facilities have released and transferred 125 million tonnes of chemicals since 2010 resulting in an estimated 24,640 years of healthy life being lost and 57 billion fractions of species being potentially affected. … BASF and Solvay are the most toxic polluters in the region, appearing in the top 5 of all four metrics analysed (physical releases, ecotoxicity, human toxicity and RSEI hazard). The financiers behind these toxic footprints are led by BlackRock (5.4% of total investments by equity market value), Vanguard (5.2%) and JPMorgan Chase (3.6%). In terms of debt financing, Citigroup leads with 6.4% of total 10-year capital underwriting (including equity, loans and bonds), followed closely by JPMorgan Chase (6.3%) and Bank of America (5.2%)“ (p. 3).

Corruption Kills: Global Evidence from Natural Disasters by Serhan Cevik and João Tovar Jalles from the International Monetary Fund as of Nov. 2nd, 2023 (#12): “… we use a large panel of 135 countries over a long period spanning from 1980 to 2020 … The empirical analysis provides convincing evidence that widespread corruption increases the number of disaster-related deaths … the difference between the least and most corrupt countries in our sample implies a sixfold increase in the number of deaths per population caused by natural disaster in a given year. Our results show that this impact is stronger in developing countries than in advanced economies, highlighting the critical relationship between economic development and institutional capacity in strengthening good governance and combating corruption“ (p. 11/12).

Investment ESG research criticsm

Complex sustainability: Sustainability of financial institutions, firms, and investing by Bram van der Kroft as of Dec. 7th, 2023 (#22): “… financial institutions will take on additional risk in ways unpriced by regulators when facing financial constraints. Throughout the paper, we provide evidence that this additional risk-taking harms society as banks and insurance corporations acquire precisely those assets most affected in economic downturns” (p. 194) … “we find for over four thousand listed firms in 77 countries, as two-thirds of firms substantively improve their sustainable performance when institutional pressure is imprecise and increases, while one-third of firms are forced to start symbolically responding” (p. 196) … “One critical assumption underlining .. sustainable performance advances is that socially responsible investors can accurately identify sustainable firms. In practice, we show that these investors rely on inaccurate estimates of sustainable performance and accidentally “tilt the wrong firms” (p. 196) … “First, we find that MSCI IVA, FTSE, S&P, Sustainalytics, and Refinitiv ESG ratings do not reflect the sustainable performance of firms but solely capture their forward-looking sustainable aspirations. On average, these aspirations do not materialize up to 15 years in the future” (p. 84). …“Using unique identification in the real estate market and property-level sustainable performance information, we find that successful socially responsible engagement improves the sustainable performance of firms”(p. 196). My comment regarding the already published ESG rating criticism: Not all rating agencies work in the criticized way. My main ESG ratings supplier shifted its focuses to actual from planned sustainability (see my Researchpost #90 as of July 5th, 2022 relating to this paper: Tilting the Wrong Firms? How Inflated ESG Ratings Negate Socially Responsible Investing under Information Asymmetries).

ESG research criticism (1)?Comment and Replication: The Impact of Corporate Sustainability on Organizational Processes and Performance by Andrew A. King as of Dec. 7th, 2023 (#186): “Do High Sustainability companies have better financial performance than their Low Sustainability counterparts? An extremely influential publication in Management Science, “The Impact of Corporate Sustainability on Organizational Processes and Performance”, claims that they do. … after reviewing the report, I conclude that its critical findings are unjustified by its own evidence: its main method appears unworkable, a key finding is miscalculated, important results are uninterpretable, and the sample is biased by survival and selection. … Despite considering estimates from thousands of models, I find no reliable evidence for the proposed link between sustainability and financial performance” (abstract). My comment: If there is no negative effect of sustainability on performance, shouldn’t all investors invest 100% sustainably

ESG research criticism (2)?Does Corporate Social Responsibility Increase Access to Finance? A Commentary on Cheng, Ioannou, and Serafeim (2014) by Andrew A. King as of Dec. 12th, 2023 (#7): “Does Corporate Social Responsibility (CSR) facilitate access to finance? An extremely influential article claims that it does … I show that its research method precludes any insight on either access to finance or its connection to CSR. … I correct the original study by substituting more suitable measures and conducting further analysis. Contrary to the original report, I find no robust evidence for a link between CSR and access to finance” (abstract).

High transition risk: The pricing of climate transition risk in Europe’s equity market by Philippe Loyson, Rianne Luijendijk, and Sweder van Wijnbergen as of Aug. 22nd, 2023 (#46): “We assessed the effect of carbon intensity (tCO2/$M) on relative stock returns of clean versus polluting firms using a panel data set consisting of 1555 European companies over the period 2005-2019. We did not find empirical evidence that carbon risk is being priced in a diversified European equity portfolio, implying that investors do not seem to be aware of or at least do not require a risk premium for the risk they bear by investing in polluting companies“ (p. 32). My comment: Apparently, at least until 2019, there has not been enough sustainable investment to have a carbon risk impact

Green indicator confusion: Stronger Together: Exploring the EU Taxonomy as a Tool for Transition Planning by Clarity.ai and CDP as of Dec. 5th, 2023: „We find that out of the 1,700 NFRD (Sö: EU’s Non-Financial Reporting Directive) companies that published EU Taxonomy reports this year, around 600 identified their revenues and spending as part of their transition plans, and approximately 300 have validated science-based targets, both of which correlate to higher taxonomy alignment overall. There is a large dispersion of eligibility across companies within similar sectors which suggests that individual companies are involved in a variety of economic activities. This influences the low correlation between corporate GHG emissions and Taxonomy eligibility and alignment, as non-eligibility can be the result of exposure to either very high-impact or very low-impact economic activities. We observe that higher taxonomy alignment does not necessarily lead to lower carbon intensity when comparing companies within sectors. It is important to highlight that the largest source of corporate emissions might not always be well reflected in revenue shares” (p. 38). My comment: My experience is that the huge part of Scope 3 CO2 emissions and almost all non-CO2 emissions like methane are still seriously neglected by many corporations and investors

Greenium:Actions Speak Louder Than Words: The Effects of Green Commitment in the Corporate Bond Market by Peter Pope, Yang Wang, and Hui Xu as of Nov. 22nd, 2023 (#64): “This paper studies the effects of green bond issuance on the yield spreads of other conventional bonds from the same issuers. A traditional view of new bond issuance suggests that new bonds (whether green or brown) will increase secondary market bond yields if higher leverage increases default risk and dilutes creditors’ claim over assets. However, we find that the issuance of green bonds reduces conventional bond yield spreads by 8 basis points in secondary markets, on average. The effect is long-lasting (beyond two years) … An event study shows that the “bond” attribute of the green bonds still increases the yield spreads of outstanding conventional bonds by 1 basis point. It is the “green” attribute that lowers the yield spreads and ultimately dominates the net effects. … we show that socially responsible investors increase their demand for, and hold more, conventional bonds in their portfolios following the issuance of green bonds … we show that shareholders submit fewer environment-related proposals following green bond issuance. … Finally, our analysis highlights that green bonds give rise to positive real effects, though such effects are confined to the issuer“ (p. 42/43).

Costly values?Perceived Corporate Values by Stefano Pegoraro, Antonino Emanuele Rizzo, and Rafael Zambrana as of Dec. 4th, 2023 (#54): “…. analyzing the revealed preferences of values-oriented investors through their portfolio holdings … Using this measure of perceived corporate values, we show that values-oriented investors consider current and forward-looking information about corporate misconduct and controversies in their investment decisions. We also show that values-oriented investors sacrifice financial performance to align their portfolios with companies exhibiting better corporate values and lower legal risk” (p. 24). My comment: According to traditional investment theories, lower (ESG or other) risk should lead to lower returns. Any complaints about that?

Some investor impact: Propagation of climate disasters through ownership networks by Matthew Gustafson, Ai He, Ugur Lel, and Zhongling (Danny) Qin as of Dec. 5th, 2023 (#127): “We find that climate-change related disasters increase institutional investors’ awareness of climate change issues and accordingly these investors engage with the unaffected firms in their portfolios to influence corporate climate policies. In particular, we observe that such institutional investors vote in greater support of climate-related shareholder proposals at unaffected firms only after getting hit by climate change disasters in their portfolios and compared to other institutional investors. … In the long-run, firm-level GHG emissions and energy usage cumulatively decline at the same time as the unaffected firms adopt specific governance mechanisms such as linking their executive pay policies to GHG emission reductions, suggesting that changes in governance mechanisms potentially incentivize firms to internalize some of the negative externalities from their activities. … our results are more pronounced in brown industries“ (p. 26). My comment: When changing executive pay, negative effects have to be mitigated, see Wrong ESG bonus math?

Other investment research

Good constraints:Performance Attribution for Portfolio Constraints by Andrew W. Lo and Ruixun Zhang as of Nov. 1st, 2023 (#57): “While it is commonly believed that constraints can only decrease the expected utility of a portfolio, we show that this is only true when they are treated as static. … our methodology can be applied to common examples of constraints including the level of a particular characteristic, such as ESG scores, and exclusion constraints, such as divesting from sin stocks and energy stocks. Our results show that these constraints do not necessarily decrease the expected utility and returns of the portfolio, and can even contribute positively to portfolio performance when information contained in the constraints is sufficiently positively correlated with asset returns“ (p. 42). My comment: Traditional investment constraints are typically used to reduce risks. Looking at a actively managed funds, that does not always work as expected. Maybe responsible investment constraints are better than traditional ones?

PE Benchmark-Magic: Benchmarking Private Equity Portfolios: Evidence from Pension Funds by Niklas Augustin, Matteo Binfarè, and Elyas D. Fermand as of Oct. 31st, 2023 (#245): “We document significant heterogeneity in the benchmarks used for US public pension fund private equity (PE) portfolios. … We show that general (Soe: investment) consultant turnover predicts changes in PE benchmarks. … we find that public pension funds only beat their PE benchmarks about 50% of the time, that they tend to use public market benchmark indices that underperform private market benchmark indices, and that their benchmarks have become easier to beat over the last 20 years“ (abstract).

Skilled fund managers: 22x new research on skyscrapers, cryptos, ESG-HR, regulation, ratings, fund names, AI ESG Tools, carbon credits and accounting, impact funds, voting, Chat GPT, listed real estate, and fintechs (# shows the SSRN full paper downloads as of Dec. 7th, 2023):

Social and ecological research

Skyscaper impact:The Skyscraper Revolution: Global Economic Development and Land Savings by Gabriel M. Ahlfeldt, Nathaniel Baum-Snow, and Remi Jedwab as of Nov. 30th, 2023 (#20): “Our comprehensive examination of 12,877 cities worldwide from 1975 to 2015 reveals that the construction of tall buildings driven by reductions in the costs of height has allowed cities to accommodate greater populations on less land. … one-third of the aggregate population in cities of over 2 million people in the developing world, and 20% for all cities, is now accommodated because of the tall buildings constructed in these cities since 1975. Moreover, the largest cities would cover almost 30% more land without these buildings, and almost 20% across all cities. …. Given the gap between actual and potential building heights we calculate for each city in our data, only about one-quarter of the potential welfare gains and land value losses from heights have been realized, with per-capita welfare gains of 5.9% and 3.1% available by eliminating height regulations in developed and developing economies, respectively. As the cost of building tall structures decreases with technical progress, such potential for welfare gains will only increase into the future. … in most cities it is in landowners’ interest to maintain regulatory regimes that limit tall building construction, … benefits may be greatest for those who would move into the city with the new construction to take advantage of the higher real wages and lower commuting costs“ (p. 47).

Hot cryptos:Cryptocarbon: How Much Is the Corrective Tax? by Shafik Hebous and Nate Vernon from the International Monetary Fund as of Nov. 28th, 2023 (#14): “We estimate that the global demand for electricity by crypto miners reached that of Australia or Spain, resulting in 0.33% of global CO2 emissions in 2022. Projections suggest sustained future electricity demand and indicate further increases in CO2 emissions if crypto prices significantly increase and the energy efficiency of mining hardware is low. To address global warming, we estimate the corrective excise on the electricity used by crypto miners to be USD 0.045 per kWh, on average. Considering also air pollution costs raises the tax to USD 0.087 per kWh“ (abstract).

ESG attracts employees: Polarizing Corporations: Does Talent Flow to “Good’’ Firms? by Emanuele Colonnelli, Timothy McQuade, Gabriel Ramos, Thomas Rauter, and Olivia Xiong as of Nov. 30th, 2023 (#48): “Using Brazil as our setting, we make two primary contributions. First, in partnership with Brazil’s premier job platform, we design a nondeceptive incentivized field experiment to estimate job-seekers’ preferences to work for socially responsible firms. We find that, on average, job-seekers place a value on ESG signals equivalent to about 10% of the average wage. … Quantitatively, skilled workers value firm ESG activities substantially more than unskilled workers. … results indicate that ESG increases worker utility relative to the baseline economy without ESG. The reallocation of labor in the economy with ESG improves assortative matching and yields an increase in total output. Moreover, skilled workers benefit the most from the introduction of ESG, ultimately increasing wage differentials between skilled and unskilled workers“ (p. 32). My comment: see HR-ESG shareholder engagement: Opinion-Post #210 – Responsible Investment Research Blog (prof-soehnholz.com)

Always greenwashing: Can Investors Curb Greenwashing? Fanny Cartellier, Peter Tankov, and Olivier David Zerbib as of Dec. 1st, 2023 (#40): “… we show that companies greenwash all the time as long as the environmental score is not too high relative to the company’s fundamental environmental value. The tolerable deviation increases with investors’ pro-environmental preferences and decreases with their penalization. Moreover, the greenwashing effort is all the more pronounced the higher the pro-environmental preferences, the lower the disclosure intensity, and the lower the marginal unit cost of greenwashing. In particular, we show that beyond a certain horizon, on average, companies always greenwash“ (p. 31).

Insufficient ESG regulation?ESG Demand-Side Regulation – Governing the Shareholders by Thilo Kuntz as of Nov. 30th, 2023 (#45): “Instead of addressing the corporate board and its international equivalents as a supplier of ESG-friendly management, demand-side regulation targets investors and shareholders. It comes in two basic flavors, indirect and direct demand-side regulation. Whereas the first attempts to let only those retail investors become stockholders or fund members who already espouse the correct beliefs and attitudes, the latter pushes professional market participants towards ESG through a double commitment, that is, to the public at large via disclosure and to individual investors through pre-contractual information. .. Judging from extant empirical studies, indirect demand-side regulation in its current form will change the equation only slightly. … for most retail investors, including adherents to ESG, .. beliefs and attitudes seem to lie more on the side of monetary gains“ (p. 49/50).

Big bank climate deficits:An examination of net-zero commitments by the world’s largest banks by Carlo Di Maio, Maria Dimitropoulou, Zoe Lola Farkas, Sem Houben, Georgia Lialiouti, Katharina Plavec, Raphaël Poignet, Eline Elisabeth, and Maria Verhoeff from the European Central Bank as of Nov. 29th, 2023 (#25): “We examined the net-zero commitments made by Global Systemically Important Banks (G-SIBs). In recent years, large banks have significantly increased their ambition and now disclose more details regarding their net-zero targets. … The paper … identifies and discusses a number of observations, such as the significant differences in sectoral targets used despite many banks sharing the same goal, the widespread use of caveats, the missing clarity regarding exposures to carbon-intensive sectors, the lack of clarity of “green financing” goals, and the reliance on carbon offsets by some institutions. The identified issues may impact banks’ reputation and litigation risk and risk management” (abstract).

ESG investment research (Skilled fund managers)

Good fund classification: Identifying Funds’ Sustainability Goals with AI: Financial, Categorical Morality, and Impact by Keer Yang and Ayako Yasuda as of Nov. 30ths, 2023 (#23): “… developing a supervised machine-learning model-based method that classifies investment managers’ stated goals on sustainability into three distinct objectives: financial value, categorical morality, and impact. This is achieved by evaluating two dimensions of investor preferences: (i) whether investors have nonpecuniary preferences or not (value vs. values) and (ii) whether investors have ex ante, categorical moral preferences or ex post, consequentialist impact preferences. … Among the funds identified as sustainable by Morningstar, 54% state they incorporate ESG to enhance financial performance, while 39% practice categorical morality via exclusion and only 33% state they seek to generate impact. Stated goals meaningfully correlate with how the funds are managed. Financially motivated funds systematically hold stocks with high MSCI ESG ratings relative to industry peers, which is consistent with ESG risk management. Morally motivated funds categorically tilt away from companies in controversial industries (e.g., mining), but are otherwise insensitive to relative ESG ratings. Impact funds hold stocks with lower ESG performance than the others, which is consistent with them engaging with laggard firms to generate positive impact. Impact funds are also more likely to support social and environmental shareholder proposals. Hybrid funds are common. Funds combining financial and moral goals are the largest category and are growing the fastest” (p. 37/38). My comment: My fund may be unique: It holds stocks with high ESG ratings, is morally motivated and tries to achieve impact by engaging with the most sustainable companies.

ESG ratings explanations:Bridging the Gap in ESG Measurement: Using NLP to Quantify Environmental, Social, and Governance Communication by Tobias Schimanski, Andrin Reding, Nico Reding, Julia Bingler, Mathias Kraus, and Markus Leippold as of Nov. 30th, 2023 (#345): “… we propose and validate a new set of NLP models to assess textual disclosures toward all three subdomains … First, we use our corpus of over 13.8 million text samples from corporate reports and news to pre-train new specific E, S, and G models. Second, we create three 2k datasets to create classifiers that detect E, S, and G texts in corporate disclosures. Third, we validate our model by showcasing that the communication patterns detected by the models can effectively explain variations in ESG ratings” (abstract). My comments: I selected my ESG ratings agency (also) because of its AI capabilities

AI ESG Tools: Artificial Intelligence and Environmental Social Governance: An Exploratory Landscape of AI Toolkit by Nicola Cucari, Giulia Nevi, Francesco Laviola, and Luca Barbagli as of Nov. 29th, 2023 (#35): “This paper presents an initial mapping of AI tools supporting ESG pillars. Through the case study method, 32 companies and tools supporting environmental social governance (ESG) management were investigated, highlighting which of the different AI systems they use and enabling the design of the new AI-ESG ecosystem” (abstract).

Cheaper green loans:Does mandatory sustainability reporting decrease loan costs? by Katrin Hummel and Dominik Jobst as of Dec. 1st, 2023 (#31): “We focus on the passage of the NFRD, the first EU-wide sustainability reporting mandate. Using a sample of global loan deals from 2010 to 2019, we begin our analysis by documenting a negative relationship between borrowers’ levels of sustainability performance and loan costs. … In our main analysis, we find that loan costs significantly decrease among borrowers within the scope of the reporting mandate. This decrease is concentrated in firms with better sustainability performance. In a further analysis, we show that this effect is stronger if the majority of lead lenders are also operating in the EU and are thus potentially also subject to the reporting mandate themselves “ (p. 26/27).

Widepread ESG downgrade costs:Do debt investors care about ESG ratings? by Kornelia Fabisik, Michael Ryf, Larissa Schäfer, and Sascha Steffen from the European Central Bank as of Nov. 27th, 2023 (#53): “We use a major ESG rating agency‘s methodology change to firms’ ESG ratings to study its effect on the spreads of syndicated U.S. corporate loans traded in the secondary market. We find that loan spreads temporarily increase by 10% relative to the average spread of 4%. … we find some evidence that the effect is stronger for smaller and financially constrained firms, but not for younger firms. We also find that investors penalize firms for which ESG-related aspects seem to play a more prominent role. Lastly, when we explore potential spillover effects on private firms that are in the same industry as the downgraded firms, we find evidence supporting this channel. We find that private firms in highly affected industries face higher loan spreads after ESG downgrades of public firms in the same industry, suggesting that investors of private (unrated) firms also price in ESG downgrades of public firms“ (p. 28).

High ESG risks: Measuring ESG risk premia with contingent claims by Ioannis Michopoulos, Alexandros Bougias, Athanasios Episcopos and Efstratios Livanis as of Nov. 9th, 2023 (#109): “We find a statistically significant relationship between the ESG score and the volatility and drift terms of the asset process, suggesting that ESG factors have a structural effect on the firm value. We establish a mapping between ESG scores and the cost of equity and debt as implied by firm’s contingent claims, and derive estimates of the ESG risk premium across different ESG and leverage profiles. In addition, we break down the ESG risk premia by industry, and demonstrate how practitioners can adjust the weighed average cost of capital of ESG laggard firms for valuation and decision making purposes“ (abstract). … “We find that ESG risk has a large effect on the concluded cost of capital. Assuming zero ESG risk premia during the valuation process could severely underestimate the risky discount rate of ESG laggard firms, leading to distorted investment and capital budget decisions, as well as an incorrect fair value measurement of firm’s equity and related corporate securities” (p. 20).

ESG fund benefits: Renaming with purpose: Investor response and fund manager behaviour after fund ESG-renaming by Kayshani Gibbon, Jeroen Derwall, Dirk Gerritsen, and Kees Koedijk as of Nov. 27th, 2023 (#42): “Using a unique sample of 740 ESG-related name changes …. Our most conservative estimates … suggest that mutual funds domiciled in Europe may enjoy greater average flows by renaming … we provide consistent evidence that mutual funds improve the ESG performance and reduce the ESG risks of their portfolios after signalling ESG repurposing through fund name changes. Finally, we find that renaming has no material impact on funds’ turnover rates or on the fees charged to investors“ (p. 15/16). My comment: Maybe I should have integrated ESG in my FutureVest Equity Sustainable Develeopment Goals fund name (ESG and more see in the just updated 31pager 231120_Nachhaltigkeitsinvestmentpolitik_der_Soehnholz_Asset_Management_GmbH).

Green for the rich?Rich and Responsible: Is ESG a Luxury Good? Steffen Andersen, Dmitry Chebotarev, Fatima Zahra Filali Adib, and Kasper Meisner Nielsen as of Nov. 27th, 2023 (#91): “… we examine the rise of responsible investing among retail investors in Denmark. … from 2019 to 2021. The fraction of retail investors that hold socially responsible mutual funds in their portfolios has increased from less than 0.5% to 6.8%, equivalent to an increase in the portfolio weight on socially responsible mutual funds for all investors from 0.1% to 1.6%. At the same time, the fraction of investors holding green stock has increased from 8.7% to 15.9%, equivalent to an increase in portfolio weight on green stocks from 2.4% to 3.3%. Collectively, the rise of sustainable investments implies that more than 4.9% of the risky assets are allocated to sustainable investments by 2021. The rise in responsible investments is concentrated among wealthy investors. Almost 13% of investors in the top decile of financial wealth holds socially responsible mutual funds and one out of four holds green stocks. Collectively, the portfolio weight on socially responsible assets among wealth investors is 4.8% in 2021. … Using investors’ charitable donations prior to inheritance, we document that the warm glow effect partially explains the documented results“ (p. 20/21).

Emissions control: Carbon Accounting Quality: Measurement and the Role of Assurance by Brandon Gipper, Fiona Sequeira, and Shawn X. Shi as of Nov. 29th, 2023 (#135): “We document a positive association between (Sö: third party) assurance and carbon accounting quality for both U.S. and non-U.S. countries. This relation is stronger when assurance is more thorough. We also document how assurance improves carbon accounting quality: first, assurors identify issues in the carbon accounting system and communicate them to the firm; subsequently, firms take remedial actions, resulting in updated disclosures, faster release of emissions information, and more positive perceptions of emissions figures by reporting firms. …. our findings suggest that even limited assurance can shape carbon accounting quality“ (p. 34).

Impact investment research (Skilled fund managers)

Carbon credit differences: Paying for Quality State of the Voluntary Carbon Markets 2023 by Stephen Donofrio Managing Director Alex Procton from Ecosystem Marketplace as of Oct. 10th, 2023: “Average voluntary carbon markets (VCM) … volume of VCM credits traded dropped by 51 percent, the average price per credit skyrocketed, rising by 82 percent from $4.04 per ton in 2021 to $7.37 per ton in 2022. This price hike allowed the overall value of the VCM to hold relatively steady in 2022, at just under $2 billion. To date in 2023, the average credit price is down slightly from 2022, to $6.97 per ton. … Nature-based projects, including Forestry and Land Use and Agriculture projects, made up almost half of the market share at 46 percent. … Credits that certified additional robust environmental and social co-benefits “beyond carbon” had a significant price premium. Credits from projects with at least one co-benefit certification had a 78 percent price premium in 2022, compared to projects without any co-benefit certification. … Projects working towards the UN Sustainable Development Goals (SDGs) also demonstrated a substantial price premium at 86 percent higher prices than projects not associated with SDGs … Newer credits are attracting higher prices” (p. 6).

Unsuccessful voting:Minerva Briefing 2023 Proxy Season Review as of November 2023: “Most resolutions are proposed by management (96.90% overall) … In 2023, there were 621 proposals from shareholders, mostly in the US (530), and mostly Social- and Governance-related (259 and 184 respectively). However, an increasing number of proposals are also being put forward on Environmental issues. The higher number of shareholder proposals in the US may reflect more supportive regulations on the filing of proposals and the absence of an independent national corporate governance code, as there is in the UK. Although well-crafted shareholder proposals can receive majority support, the overall proportion doing so has decreased (5.80% in 2023 vs. 11.56% in 2022), partly dragged down by ‘anti-ESG’ proposals” (p. 3/4). My comment: 621*6%=37 majority supported shareholder proposals including non ESG-topics seems to a very low number compared to the overall marketing noise asset managers produce regarding their good impact on listed companies. Direct shareholder engagement with companies seems to have more potential for change. My respective policy see Shareholder engagement: 21 science based theses and an action plan – (prof-soehnholz.com)

Good impact returns:Impact investment funds and the equity market: correlation, performance, risk and diversification effects – A global overview by Lucky Pane as of July 2021: “Impact investing funds from the twelve economies reported an average return of 10.7% over the period 2004-2019, higher than the average return of the MSCI World Equity Index (8.7%). … Negative/low correlations were observed between impact investment funds and traditional assets of the following countries: Germany, Australia, UK, Brazil, China, Poland, South Korea and Turkey” (p. 35/36). My comment: Unfortunately, there are very few (liquid) impact investing studies. A study including 2022 and 2023 would come to less favorable return conclusions, though.

Other investment research

Skilled fund managers (1): Sharpening the Sharpe Style Analysis with Machine-Learning ― Evidence from Manager Style-Shifting Skill of Mutual Funds by George J. Jiang, Bing Liang, and Huacheng Zhang as of Dec. 3rd, 2023 (#38): “Nine out of 32 indexes are selected as the proxy of style set in the mutual fund industry. We … find that most active equity funds are multi-style funds and more than 85% of them allocate capitals among three to six styles. Single-style funds count less than 3% of the total number of funds. We further find that around 3% of funds shift their investment styles in each quarter and each shifting fund switches styles three times over the whole period … We find that shifting funds perform better in the post-shifting quarter than in the pre-shifting quarter in terms of both total returns and style-adjusted returns, but we do not find performance improvement by non-shifting funds. We further find that style-shifting decision is positively related to future fund returns. … We find that style-shifting in the mutual fund industry is mostly driven by fund managers’ expertise in the new style“ (p. 42).